US stocks are poised for their first weekly decline since March as the AI stock rally cools ahead of the May jobs report, according to market watchers [1]. On June 5, Asian tech shares fell sharply, mirroring US losses after Broadcom disappointed investors with a weak AI revenue outlook and missed earnings expectations [2, 3, 1].

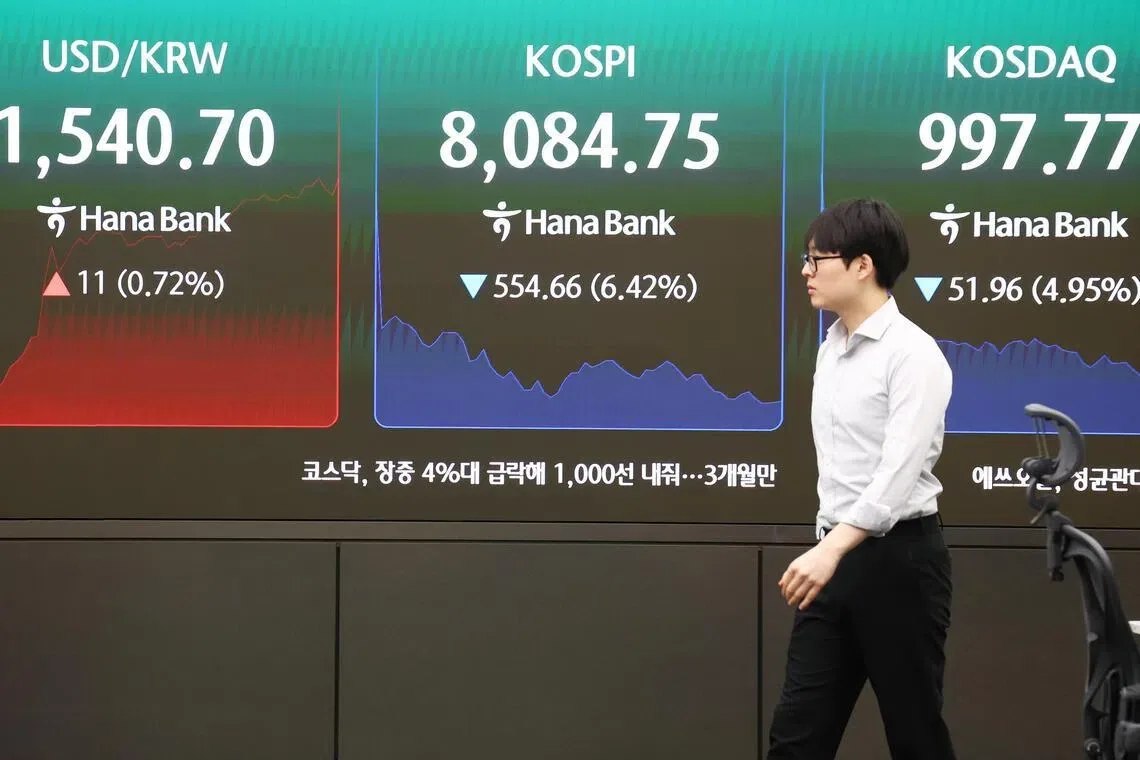

South Korea’s Kospi index dropped 5.3%, reversing some of its 105% gains this year, with key tech names Samsung Electronics and SK Hynix seeing steep share declines. SK Hynix shares fell 8.9% following Broadcom’s revenue shortfall, while Samsung declined alongside the broader selloff [2, 3]. Broadcom shares had slumped 12.6% on June 4 after missing revenue targets, triggering worry across the AI semiconductor sector [2].

MSCI’s Asian equities gauge declined 1.6% on June 5, while Japan’s Nikkei slipped 1.6%. Nasdaq 100 futures fell between 1% and 1.3% for a third straight day, according to differing market sources [2, 3]. Charu Chanana, chief investment strategist at Saxo, said, “Korea has been one of the biggest beneficiaries of the AI memory supercycle, so when Broadcom disappointed on AI expectations, investors quickly de-risked the whole semiconductor chain” [2].

Despite the selloff, some analysts remain optimistic about the AI sector’s longer-term prospects. Jung In Yun, CEO at Fibonacci Asset Management Global, noted, “Valuations in parts of the AI ecosystem have become stretched. Near-term volatility is likely to remain elevated, though we do not view this as a change in the broader trend” [2]. Jonathan Pines, head of Asia ex-Japan equities at Federated Hermes, remarked, “The market breadth is indeed narrow, but that will not necessarily stop the benchmark from hitting 10,000” [2].

Meanwhile, Nvidia certified Samsung, SK Hynix, and Micron to supply advanced high-bandwidth memory products needed for its AI accelerators, signaling ongoing industry collaboration despite market jitters [1]. In other news affecting tech capital flows, underwriters of the upcoming SpaceX IPO were instructed not to accept orders from Hong Kong and Chinese investors due to US export controls on critical technology [1].

The May jobs report, due on Friday, remains a key near-term data point for investors assessing US economic momentum and market direction [1].