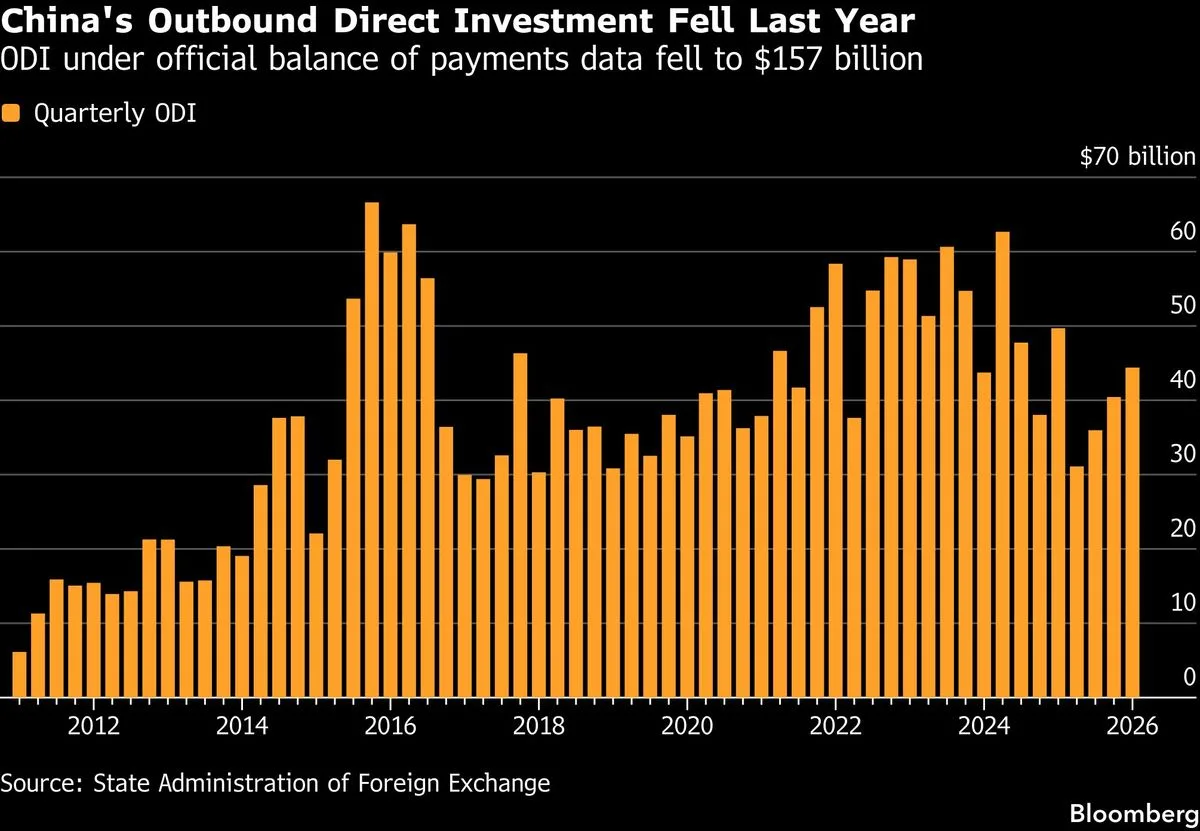

China's cabinet released new rules on June 1, 2026, that broaden outbound investment regulations to explicitly include individual investors for the first time, marking a significant policy shift [1, 2, 3]. Previously, outbound direct investment approval was only required from Chinese firms investing overseas; individual investors had operated in an ambiguous legal space [1, 2, 3]. Wang Zhiyi, founder of Shanghai Fangchang Information Development Co., said, "Strictly speaking, China has long lacked a systematic institutional framework for outbound direct investment by individual domestic residents" [1].

The updated rules widen the definition of "investors" to cover individual residents, aiming to curb capital outflows via offshore channels historically used by entrepreneurs and wealthy Chinese moving assets abroad through acquisitions, overseas property purchases, and stakes in foreign companies [1, 2]. Gene Ma, head of China Research at the Institute of International Finance, explained, "The capital subsequently raised through offshore IPOs is not necessarily repatriated, but is instead retained overseas, creating a massive external capital loop. By bringing individuals into the regulatory framework, China hopes to better manage this situation" [2].

Regulators have already acted against companies facilitating unauthorized outbound securities business. In May 2026, authorities fined Futu, Longbridge, and Tiger Brokers over US$330 million and ordered a two-year rectification period including winding down their mainland China operations [4, 5]. Mainland Chinese investors are now shifting assets from such sanctioned brokers to mainland-approved channels and Hong Kong–licensed brokers amid the crackdown [4, 5]. Estimated offshore financial assets held by mainland Chinese individuals in US and Hong Kong stocks total roughly US$54 billion, according to Kaiyuan Securities [5].

Meanwhile, the Hong Kong Monetary Authority stated on June 6 that mainland Chinese clients may continue to open bank accounts in Hong Kong, but banks must implement stringent compliance checks in line with new regulatory requirements. The HKMA said, "Chinese mainland customers continue to apply for opening accounts, and in general, the account opening process has been operating smoothly" [6].

The new outbound investment rules do not yet specify the detailed supervision mechanisms for individual investors; those will be developed later by relevant government departments [1, 2]. Meanwhile, some individual investors are wary of increased restrictions. Shenzhen-based AI engineer Sihan Wang commented, "I would rather step back now than risk having my funds caught up in future restrictions" [4].