The Japanese yen's real effective exchange rate dropped to its lowest point since the 1970s, marking a half-century low in the currency's purchasing power [1, 2, 3, 4]. On May 23, Robin Brooks of the Brookings Institution said the yen's rate is now weaker than the Turkish lira, making it the weakest currency globally by this measure [1, 2].

The yen faces structural downward pressure caused largely by a widening trade deficit driven by high international oil prices. Elevated energy costs have increased Japan's import expenses, contributing to the forecasted trade deficit widening to about 5 trillion yen in 2026 [1, 2, 3, 4, 5]. As Miyamae Koya, senior economist at SMBC Nikko Securities explained, "Due to high international oil prices, Japan's trade deficit may expand to about 5 trillion yen, pressuring the yen to depreciate" [1].

Japan’s government is responding with fiscal measures. Prime Minister Sanae Takaichi announced plans to compile a supplementary budget exceeding 3 trillion yen for fiscal 2026 to subsidize fuel and utilities costs [1, 2]. At the same time, the Bank of Japan continues its accommodative monetary policy. Takeda Jun, chief economist at Itochu Research Institute, said, "Pursuing expansive fiscal policy alongside accommodative monetary policy lowers confidence in the yen and brings selling pressure" [1].

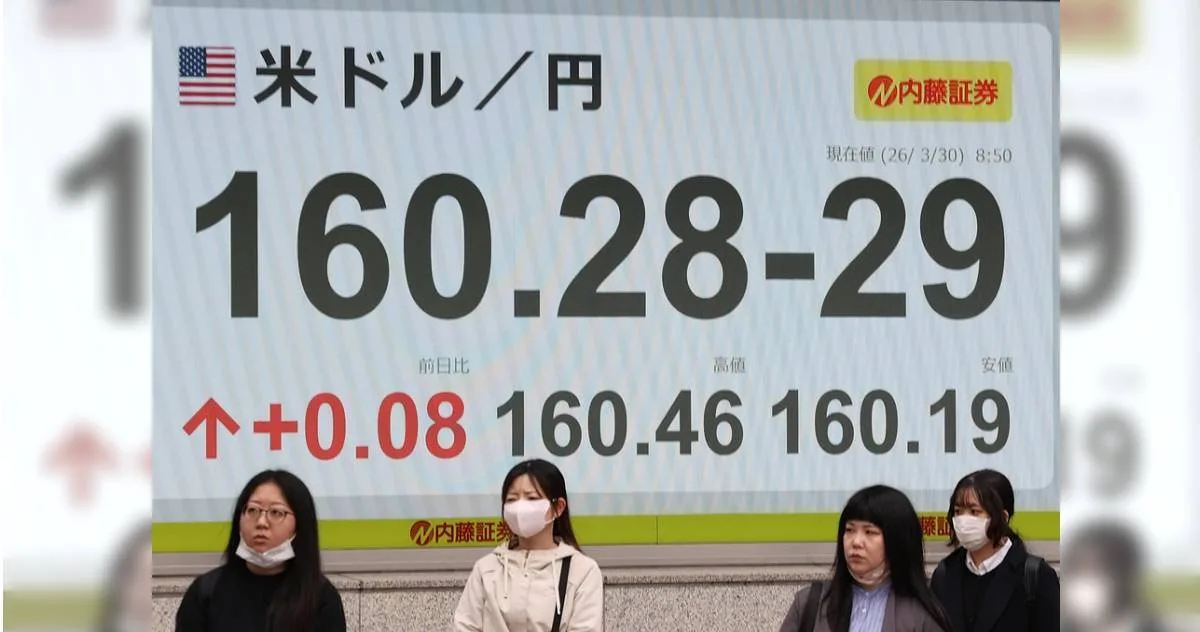

Since April 28, the Japanese government and central bank have intervened heavily in foreign exchange markets. They spent about 11.7 trillion yen (roughly $730 billion) trying to support the yen after it fell below 160 yen per US dollar, the intervention trigger point [3, 4, 5]. Despite this, the yen remained near the 160-yen level, with a brief dip to 159.38 yen on May 29 renewing market concerns [2, 3, 4, 5]. Tokyo Branch Head at State Street Bank, Tokubei Watanabe, said, "If the exchange rate falls below 160 yen, we expect the government to intervene again" [4].

However, concerns are growing about the limits of intervention. Japan holds about 1 trillion USD in foreign exchange reserves, which theoretically allows for about 30 rounds of intervention. Yet, experts warn that continuous use of reserves may lose effectiveness and raise doubts about market confidence and diplomatic relations. Daisaku Ueno, chief FX strategist at MUFG Securities, cautioned, "The more reserves Japan uses up, the more vulnerable it appears to speculators" [5].

The yen’s purchasing power remains under pressure, and further intervention is likely if the exchange rate weakens beyond key thresholds. The government’s supplementary budget for fuel and utilities subsidies is expected to be finalized for fiscal 2026.