Iran closed the Strait of Hormuz on February 28, 2026, causing tanker crossings to fall sharply from about 46 daily before the war to fewer than two per day on average during March 2026 [1, 2, 3]. This passage carries about one-fifth of the world's crude shipments, which nearly collapsed overnight after the closure [1, 2, 3].

On April 13, US enforcement actions further limited commercial tanker operations in Iranian waters, making the area largely inaccessible to most operators [1, 2, 3]. Tehran signaled a reopening on April 17, leading to a brief surge to 16 tanker crossings on April 18—about one-third of normal volume—but this window closed within 24 hours after the USS Spruance reportedly seized the tanker Touska on April 19, causing crossings to drop back to around two per day [1, 2, 3].

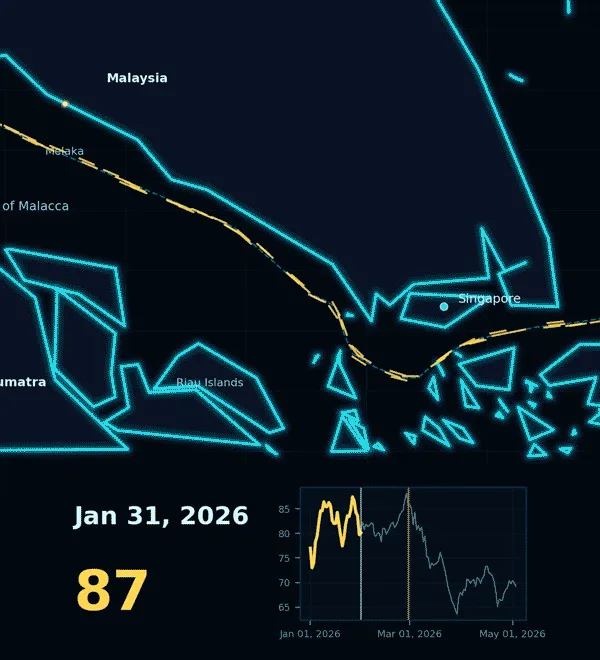

Meanwhile, tanker traffic through the Strait of Malacca, a key route linking alternative crude sources such as West Africa and North America to North Asia, fell from a pre-war average of 83 daily crossings to about 71, a 14% decline after the Hormuz closure [1, 2, 3]. This route partially offset the disruption caused by the Hormuz shutdown.

Higher oil prices driven by the Hormuz disruption have started to affect industrial production and global consumer demand, though current impacts remain modest [1, 2, 3]. For Singapore, an important trading and refining hub, the conflict has not posed an immediate risk, but prolonged disruption could reduce tanker flows through the region [1, 2, 3].

A rare tanker crossing occurred on May 13, when the Chinese supertanker Yuan Hua Hu passed through the Strait of Hormuz, one of few such voyages since the crisis began [1, 2, 3].