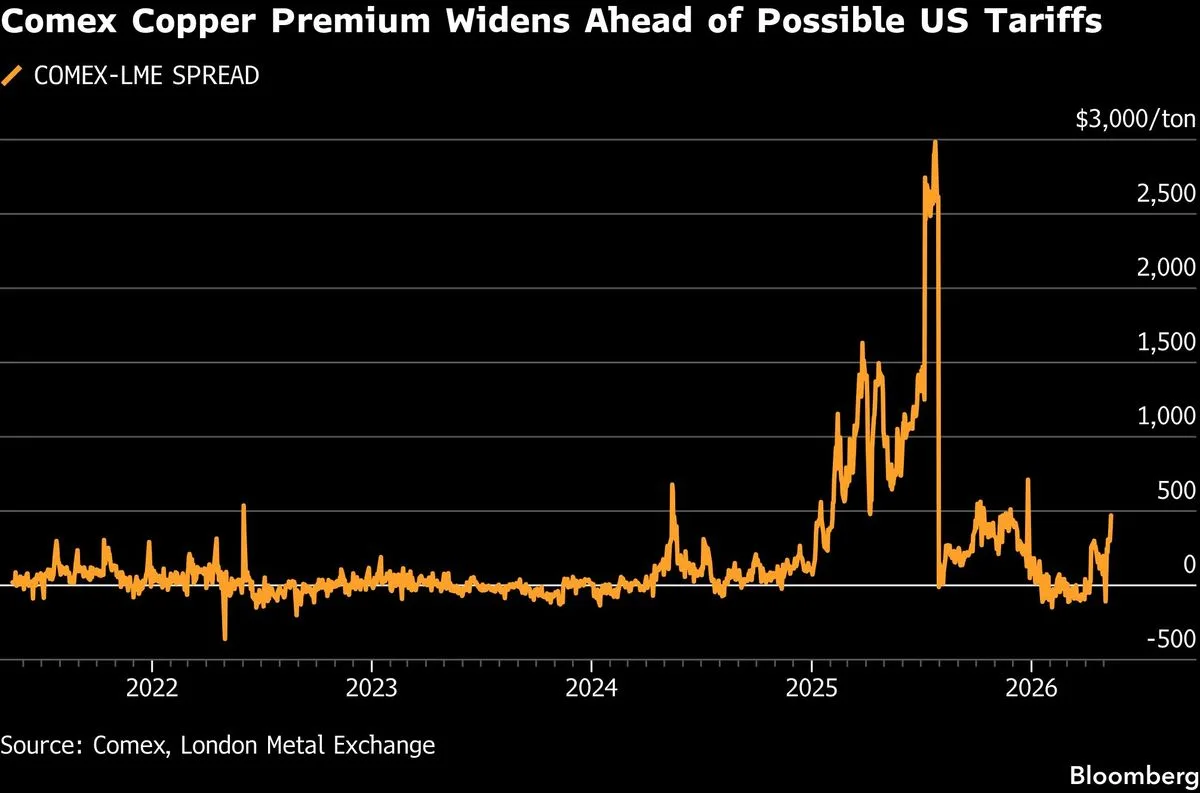

Copper prices rose to record or near-record levels on May 13 as global supply tightened and demand stayed firm. The London Metal Exchange contract touched US$14,196.50 a tonne, while U.S. Comex copper was at US$6.69 a pound, as traders also priced in expected U.S. tariffs on refined copper imports. [1]

Supply disruptions at major mines helped drive the shortage. In February, a fire hit Kamoa-Kakula in the Democratic Republic of Congo. Cobre Panama remained shuttered after a court ruling in 2023. In Peru, blockades at Las Bambas and problems at Antamina have weighed on output. Chinese smelters have also faced raw material shortages, while sulfuric acid supplies from the Middle East have been constrained by the Iran conflict and disruption in the Strait of Hormuz. [1, 2]

Demand has stayed strong. Copper is used heavily in electrification, and China continues to consume large volumes. China’s refined copper output reached 1.05 million tonnes in April, down 3% from March, but still pointed to a market that has not caught up with demand. Li Xuezhi, head of research at Chaos Ternary Futures Co., said, “The slew of supply issues combined with solid demand is leading industrial metals to recover notably as worries over the Iran war ease.” [1]

Forbes reported on May 11 that copper had hit an all-time high as outages and shortages spread through the market, and said the metal was trading at US$6.44 a pound on Comex. The report also said mining stocks were benefiting, with BHP shares up 25% in six weeks and 56% over 12 months. Rio Tinto was also among the apparent winners from the rally. [2]

Copper had already set an earlier all-time high on the London Metal Exchange in January, when the market first pushed to US$14,527.50 a tonne. The latest trading left the metal just below that peak, with prices still near historic highs as supply problems persisted. [1]