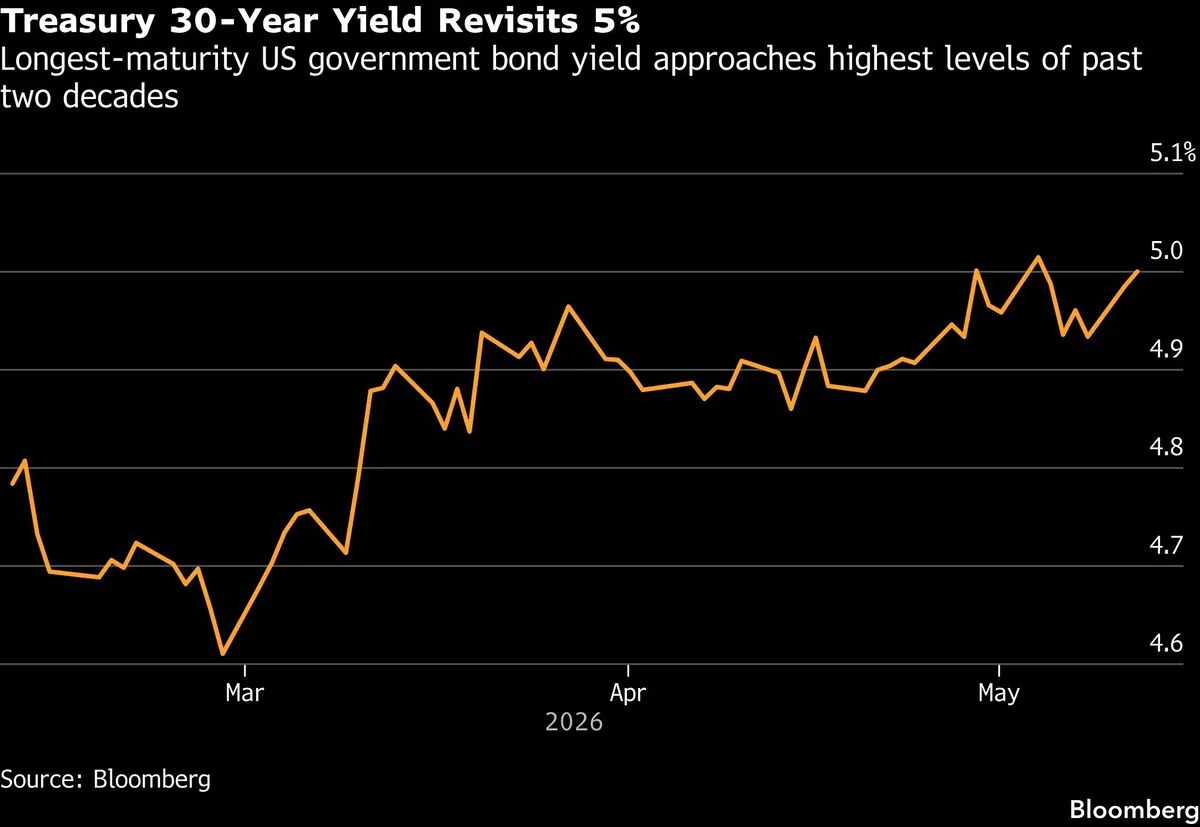

US Treasury yields rose by 2 to 5 basis points near mid-day trading on May 12, with the 30-year yield reaching around 5%, marking a sustained rise amid inflation and oil price pressures [1, 2]. Benchmark oil prices climbed more than 3% due to the ongoing US conflict with Iran, which has disrupted Middle East oil supply and tightened global markets [1].

Inflation data released for April 2026 showed the US consumer price index (CPI) increased 3.8% year-on-year, the fastest pace since 2023, further strengthening the case for Federal Reserve interest rate hikes [2]. Excluding volatile food and energy costs, core CPI rose 0.4% month-on-month and 2.8% year-on-year, exceeding economists’ forecasts [2].

Zachary Griffiths, head of investment grade and macro strategy at CreditSights, said, “It’s an ugly print but generally seems to be matching expectations, limiting the immediate market impact. There’s little in terms of relief in the underlying inflation trends, and we are more concerned that yields may remain elevated for longer.” [2]

Traders in interest rate swaps currently price in about a 70% chance of a quarter-point Fed rate increase by April 2027, reflecting heightened caution over inflation risks [2]. Meanwhile, an upcoming $42 billion auction of 10-year Treasury notes is expected to show yields around 4.45%, higher than previous auctions since February 2025 [2].

Across the Atlantic, UK government bond yields also rose sharply on May 12, driven by political uncertainty surrounding Prime Minister Keir Starmer's leadership, with gilt yields increasing by 8 to 11 basis points [2].

The next major event for the US Treasury market will be the 10-year note auction planned soon, where investors will gauge demand and yields amid persistent inflation and geopolitical tensions.