The People’s Bank of China (PBOC) has instructed major state-owned banks, including policy banks, to strictly limit their net lending to other banks in the interbank market. The directive began circulating recently as a measure to manage a months-long glut of liquidity pushing borrowing costs to multi-year lows and distorting market signals [1, 2, 3, 4].

This informal directive, known as window guidance, aims to prevent interbank borrowing costs from falling too far below the central bank’s policy interest rate and to reinforce the authority of the benchmark rate. The PBOC uses this tool to steer money market rates amid periods of volatility and to control the pace of credit extension [1, 3, 4].

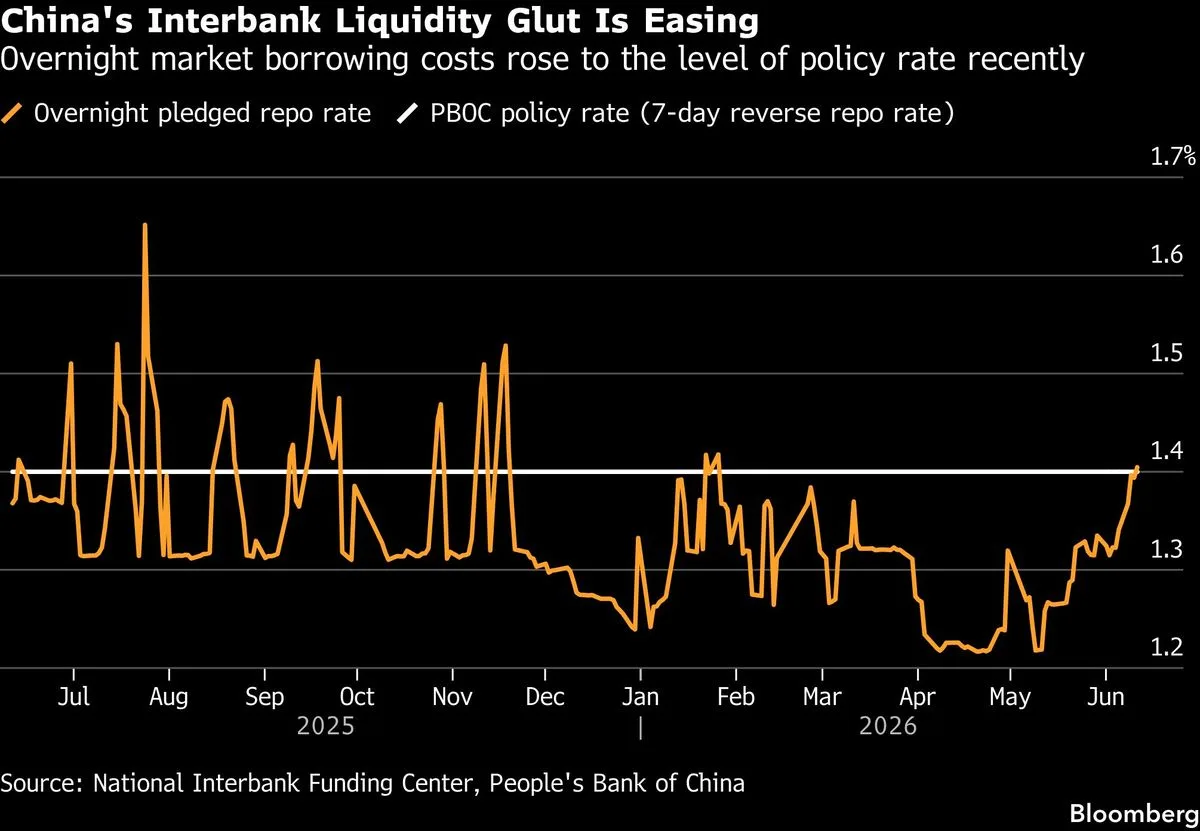

The liquidity surplus has driven the overnight repo rate down to around 1.2% in April. However, intervention has helped push it back up to about 1.4% in early June, matching the policy benchmark rate. Meanwhile, yields on 10-year government bonds climbed to 1.75% from 1.7% earlier in June, reflecting the influence on financial markets [1, 2, 3, 4].

The central bank is balancing the need to provide enough liquidity to support economic growth with the risk that excess funds circulating within the financial system could fuel asset bubbles. Weak demand for borrowing from businesses and households has led banks to increase lending to each other or buy more government and policy financial bonds, further adding to liquidity pressures [1, 2, 3, 4].

Credit growth slowed to its weakest pace on record, intensifying excess liquidity tensions within the banking system. By curbing interbank lending, the PBOC seeks to restrain the flow of funds and maintain orderly market conditions [1, 2, 3, 4].

Reports detailing the PBOC’s instructions emerged on June 12, shedding light on the central bank’s approach to addressing the liquidity imbalance caused by subdued credit demand and market conditions [1, 2, 3, 4].