China's economy in April 2026 displayed a clear K-shaped growth pattern, with industrial production growing strongly but consumer spending remaining weak, according to economic data released this week [1, 2].

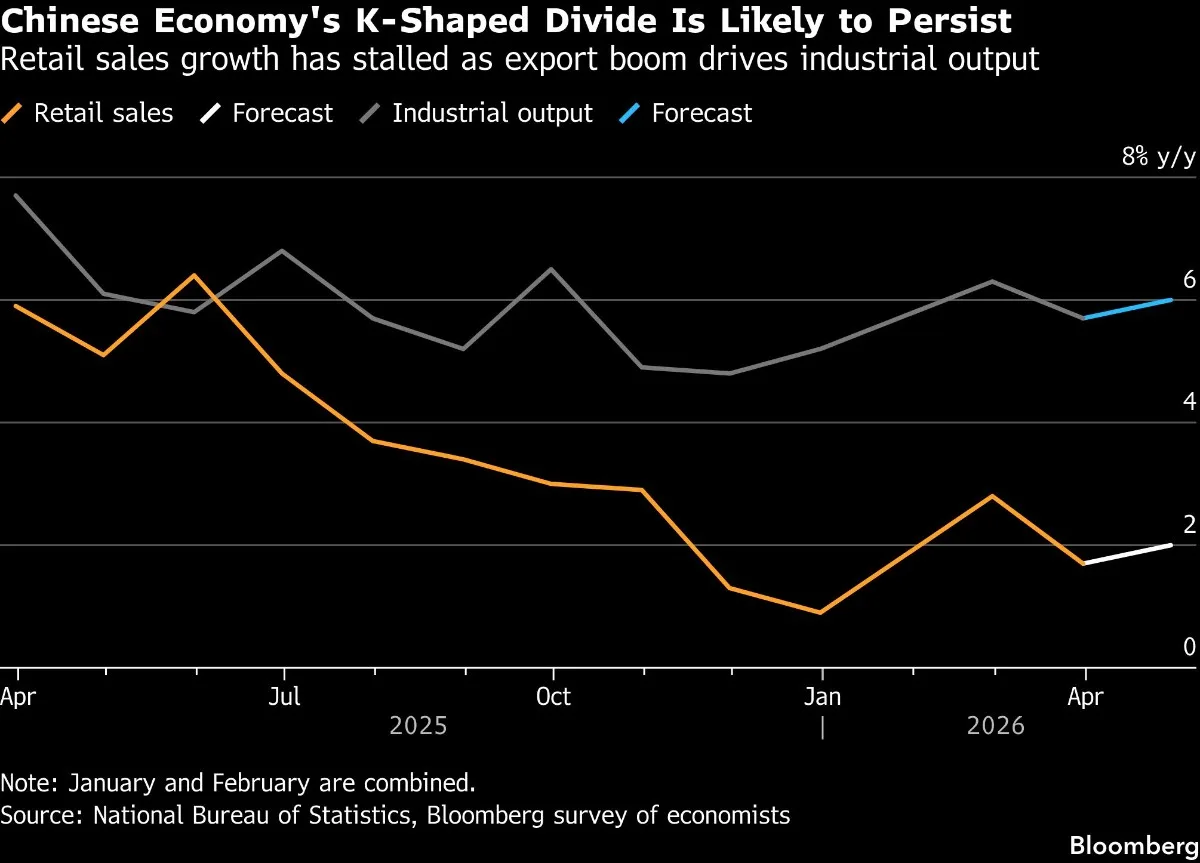

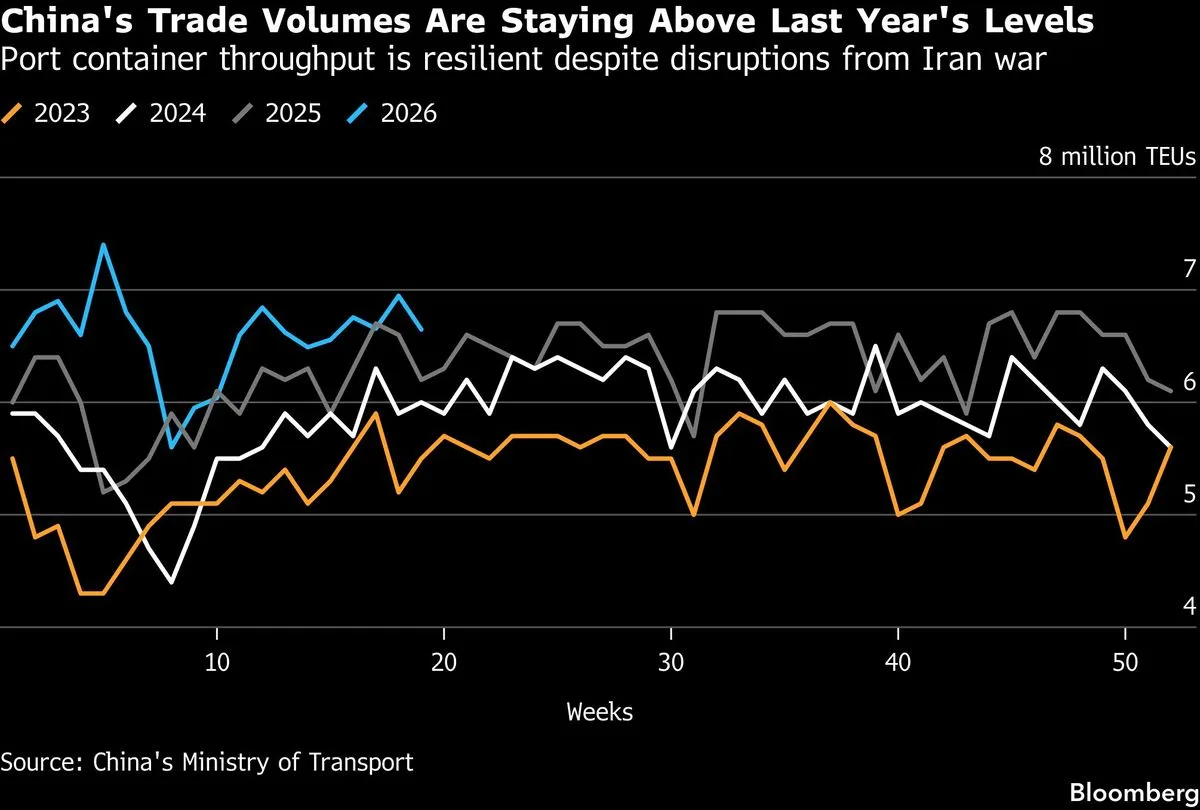

Industrial production expanded by 6.0% year-on-year in April, up from 5.7% growth in March. This highlights continued strength in the manufacturing and production sectors amid global demand [1, 2]. Exports surged 14.1% year-on-year, aided by increased global investment in artificial intelligence and high demand for renewable energy products, a trend intensified by disruptions in Middle East energy supplies [1, 2]. Stabilizing trade relations with the United States, potentially supported by former President Donald Trump's recent visit to Beijing, contribute to a positive outlook for exports [1, 2].

In contrast, retail sales showed modest growth of 1.9% year-on-year in April, a slight increase from 1.7% in March, but still one of the slowest annual starts outside the pandemic period. This sluggish consumer demand signals ongoing weakness in domestic spending [1, 2]. Citigroup economists led by Xiangrong Yu said, "We expect the K-shaped divergence to extend into April. Industrial production remains buoyant but that’s contrasting with sluggish domestic demand" [1].

Chinese policymakers appear cautious about intervening further in the K-shaped growth gap after years of efforts to boost consumer spending have yielded limited results [1, 2]. Chronic weakness in the jobs market and an unresolved property crisis are major barriers to reviving household confidence and spending [1, 2]. The government also reduced fiscal spending in March 2026, and the People's Bank of China has so far refrained from further monetary easing despite ample liquidity and weak credit demand [1, 2].

In March 2026, the Chinese government cut back on fiscal outlays while the central bank held off on signaling policy changes, setting the stage for the mixed performance seen in April [1, 2]. The April figures confirm a two-speed economic recovery with manufacturing and exports outperforming consumer sectors.

China’s economic trajectory now hinges on addressing the domestic demand shortfall amid a strong industrial base and surging exports. The next major data release set for May 2026 will indicate whether consumer spending picks up or remains sluggish in the second quarter [1, 2].