Yields on US Treasury bonds climbed to multiyear highs in mid-May 2026, with the 10-year yield reaching about 4.54% and the 30-year yield hitting 5.18%, levels not seen since around 2007 [1, 2, 3]. The bond selloff intensified on May 19 as large block sales of US Treasury futures worth around $15 billion worsened market volatility and pushed yields higher [4, 5].

The surge in yields is driven primarily by accelerating inflation fears sparked by rising oil prices. Brent crude prices climbed above $107 a barrel amid ongoing disruptions tied to the US and Israel’s war against Iran, which began in early March 2026 and effectively closed the Strait of Hormuz, a vital oil transit route [1, 3, 6, 7]. Prashant Newnaha of TD Securities warned, "An extended and persistently high oil price could be the nail in the coffin for bonds" [6].

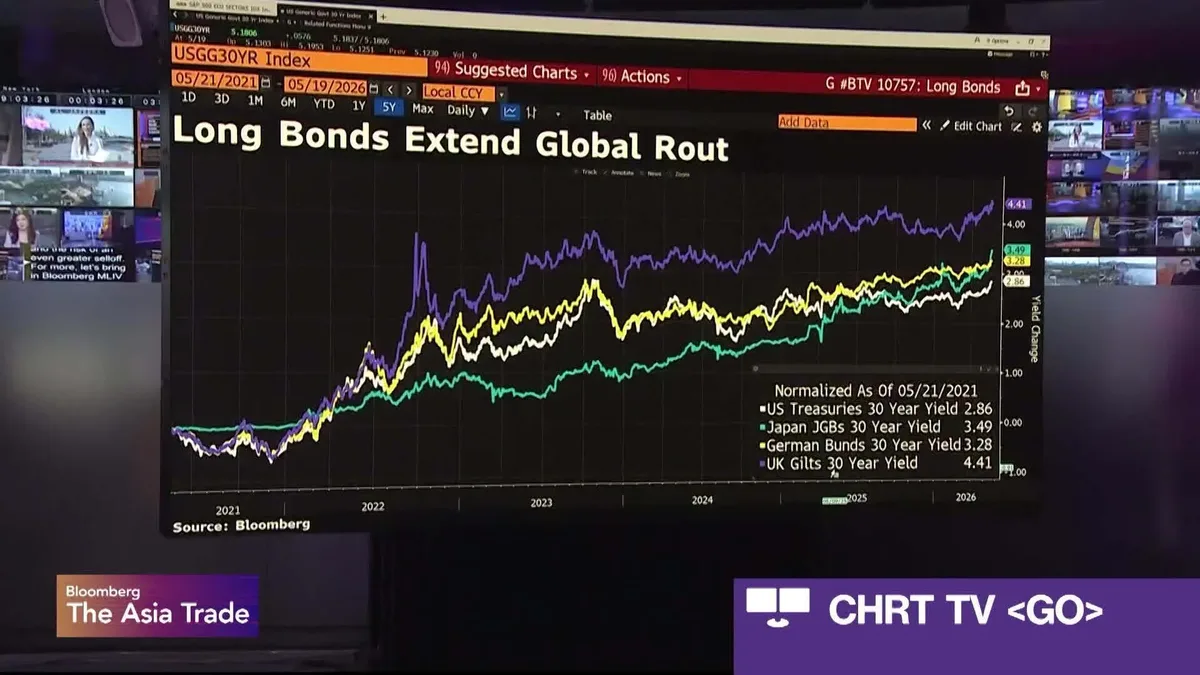

The selloff is broad based, impacting sovereign debt markets across the US, UK, Eurozone, Japan, Australia, and New Zealand [1, 3, 6]. Japan’s government bonds also surged sharply, with the 20-year yield hitting levels last seen in 1996 at around 3.7%-3.71%, and the 30-year yield reaching about 4.0%—the highest since it was issued in 1999 [8, 9, 10, 6]. Foreign investors sold a net ¥81.3 billion (approximately $512 million) of Japan’s super-long bonds in April 2026, the first net sale since December 2024 [9].

Investors have unwound carry trades due to rising yields and inflation fears, causing increased volatility and a "flush out" in bond markets, Stephen Spratt of Societe Generale said [6]. Federal Reserve officials’ hawkish comments and market pricing of possible rate hikes into 2027 added pressure on yields [6, 11]. Ajay Rajadhyaksha of Barclays noted, "With debt rising faster than growth, worsening inflation profiles, and no political will for fiscal reform, there is little reason to reach for the long end" [11].

Besides inflation and war, rising fiscal deficits and government spending in major economies contribute to higher yield demands. The International Monetary Fund projects global public debt will rise to 100% of GDP by 2029, up from about 95% currently, raising concerns over long-term debt sustainability [7]. Demographic trends, supply chain shifts, and green infrastructure investments may keep inflation and interest rates elevated over the longer term, according to IMF analysis [7].

The UK pound weakened sharply to its worst level since 2024 amid inflation worries and political instability, including challenges to Prime Minister Keir Starmer’s leadership [12, 7]. The recent summit between Donald Trump and Xi Jinping emphasized stronger US-China ties despite global uncertainties [12].

On May 20, Japan’s 20-year bond auction showed firm demand, causing yields to dip slightly but remain near multidecade highs [9, 10]. Global markets will watch upcoming central bank meetings closely as investors price in future policy moves amid persistent inflation and geopolitical risks.