SpaceX, OpenAI, and Anthropic are planning initial public offerings in the US that are expected to raise about $70 billion combined, according to reports today. The capital raised could fuel a new wave of technology spending benefiting Asian suppliers of server parts, specialized materials, cooling components, and power equipment [1, 2, 3].

This potential influx of funds would add to the more than $750 billion that large hyperscalers have already committed to AI-related capital expenditures, accelerating the buildout of data center infrastructure and hardware supply chains in Asia [2, 3].

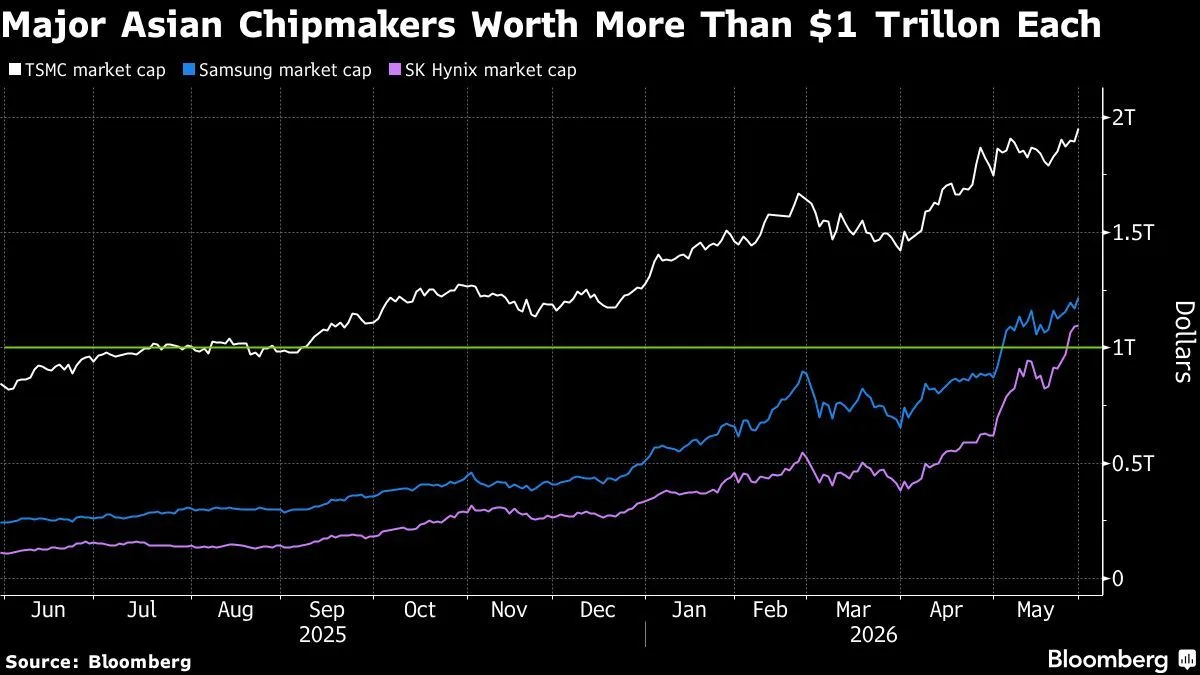

Companies such as Taiwan Semiconductor Manufacturing Co, Samsung Electronics, SK Hynix, Samsung Electro-Mechanics, and Japan’s Ibiden have been major beneficiaries of the ongoing data center construction and are currently among the biggest winners in this sector [2, 3].

However, some investors express caution regarding the high valuations of pure semiconductor companies. Instead, they are shifting focus to electronic component manufacturers and specialized suppliers seen as the next class of AI winners in Asia. "AI IPOs could further fuel the capex boom at a time when Asian chip stocks look stretched. We’re currently underweighting semiconductors in our Asia technology strategy and focusing more on the electronic component makers," said Ken Wong, Asian equity portfolio specialist at Eastspring Investments [2].

The AI spending and semiconductor expansion is driving gains not only in chips but also in server components, advanced packaging, chip testing, optical communication, power equipment, and cooling technology sectors, noted Song Zhe, asset manager at BNP Paribas Investment Partners. "The next wave will focus on specific stocks rather than the whole semiconductor group," he added, highlighting focus areas including Taiwan and China firms involved in advanced packaging, substrates, and cooling techniques [2, 3].

Power supply for AI data centers, in particular, is growing as a bottleneck. Investors are showing interest in companies related to transformers, fuel cells, cables, and gas turbines. "Power is currently the lowest held but most important bottleneck in the market," said Jian Shi Cortesi, fund manager at Gam Investment Management [3].

Beyond chips and hardware, some investors are also betting on AI applications outside of chatbots, including robotics and autonomous vehicles. These sectors could lift stocks such as LG Electronics [3].

The reports of SpaceX, OpenAI, and Anthropic’s planned IPOs today have sharpened investor focus on the Asian AI supply chain. The additional capital spending from these listings is expected to extend the AI capital expenditure cycle for years. "Investors are likely to seek companies that can benefit directly but still have relatively cheap valuations," said portfolio manager Sam Konrad at Jupiter Asset Management [3].