The US Labor Department reported a 172,000 increase in nonfarm payroll employment in May, surpassing market forecasts, with the unemployment rate steady at 4.3% [1, 2, 3, 4]. Average hourly wages rose 0.3% month-on-month and 3.4% year-on-year, led by gains in government and leisure/hospitality sectors [3, 4]. The robust job data showed no signs of impact from ongoing Middle East tensions [3, 4].

The strong payroll growth sharply raised expectations that the Federal Reserve will maintain a tightening stance. Market pricing implies a 4.6% chance of a 25 basis point rate hike at the upcoming June 17 Fed meeting and a 42.7% chance of a hike by December [2]. Newly appointed Fed Chair Kevin Warsh will preside over the June 16-17 meeting amid heightened inflation concerns. Heather Long, Navy Federal Credit Union's chief economist, said Warsh "must act firmly on inflation or risk losing bond market trust" [1].

The US equity market reacted negatively. On June 5, the Nasdaq index plunged 4.18%, the S&P 500 fell 2.64%, and the Dow dropped 1.35%—ending nine weeks of gains [2, 5]. Technology stocks, especially semiconductors, led the decline with the Philadelphia Semiconductor Index dropping over 10% [2]. Analyst Ryan Detrick of Carson Group noted, "The strong jobs report puts the Fed in a dilemma about cutting rates this year, and markets have sold off this year's best-performing sectors to vent." Gold also dropped sharply amid risk-off sentiment [2]. Treasury yields rose, with the 2-year up 10 basis points to 4.14%, and the 10-year yield rising to 4.54% [3, 4].

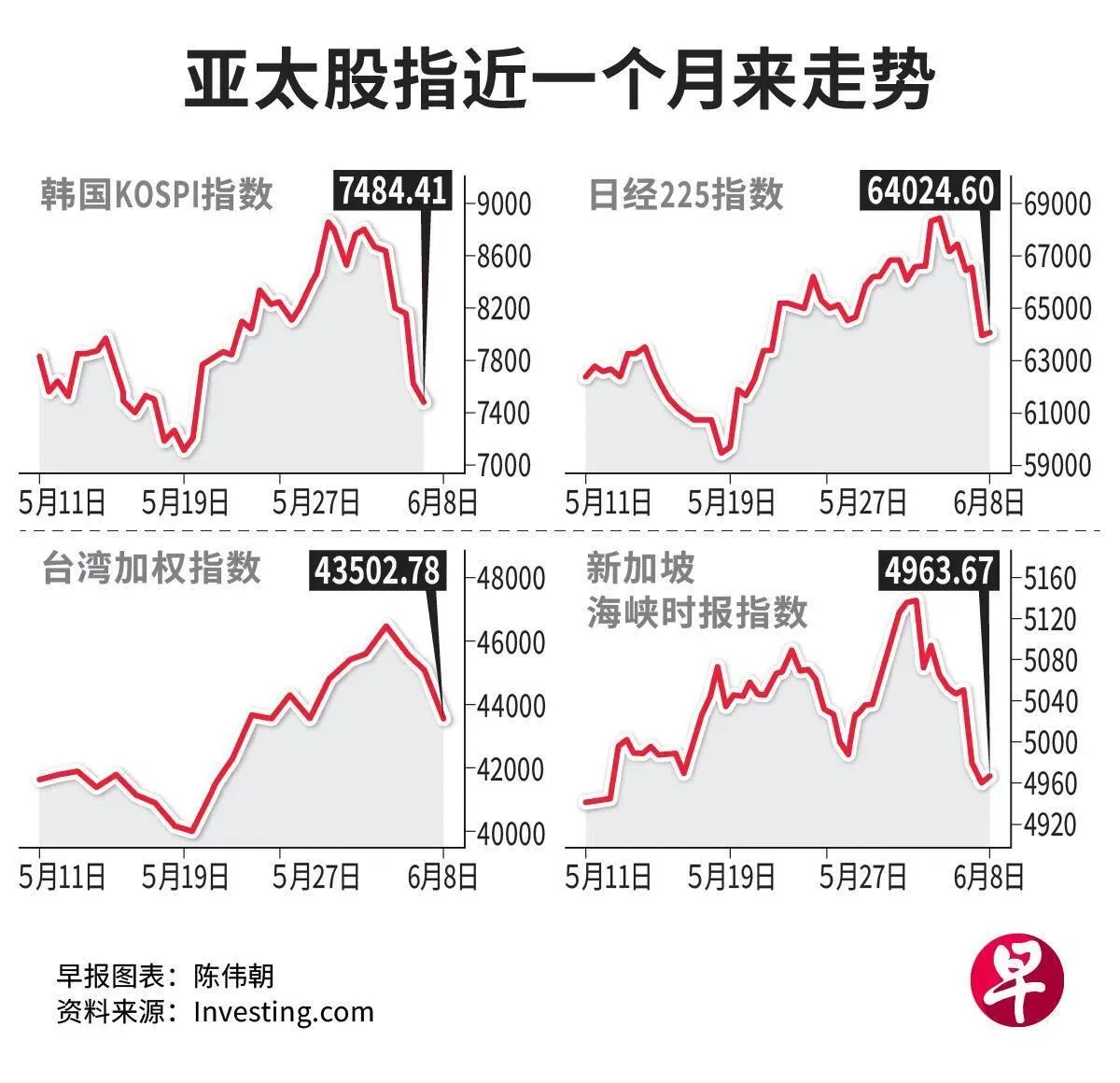

The US job data ripple hit Asian markets on June 8, as concerns about Fed tightening sparked sell-offs. Taiwan's market dropped 5.39%, Hong Kong and China indices fell over 1%, and Singapore's Strait Times index declined 1.38%, driven by weakness in AI and tech stocks [6, 7]. South Korea’s KOSPI plunged 8.29%, triggering a trading halt [8]. Charu Chanana, Saxo Bank strategist, called these declines "just a trigger" driven by crowded AI trades, dominance of a few AI leaders, investor worries over AI funding, and geopolitical risks. Hu You of FSM Global described the moves as "a sharp correction in the AI-driven bull market but not the start of a long-term bear market" [8].

Asian markets rebounded on June 9 after easing Middle East tensions and a stabilization in AI stocks. Singapore’s index rose 1.2%, South Korea gained over 4%, while Japan and Taiwan also climbed [9, 10, 11].

The next closely watched event is the Federal Reserve meeting on June 16-17, with investors awaiting guidance on monetary policy under Chair Kevin Warsh amid ongoing inflation and market volatility [1].